Guide

A guide to company credit checks

Read this guide to understand:

✅ What a company credit check means

✅ How to run company credit checks

✅ Why they’re important for your business

Read this guide to understand:

✅ What a company credit check means

✅ How to run company credit checks

✅ Why they’re important for your business

Checking your own business credit score is an obvious step for many, it can open doors to affordable finance, better terms, or winning new business. But did you know that the credit scores of other companies can also affect you?

Late payments are regrettably too common, and if delays occur within your supply chain, it can have a significant impact. However, credit checking the companies you work with can help to mitigate these risks.

Skip to:

A company credit check is a report of another business’ creditworthiness. It will include important information, such as the business’ credit score, their suggested credit limit, credit history, public records, CCJs registered and other data on their financial health.

Credit checks allow other businesses, be it a lender, supplier, a partner, or customer of the company, to assess the level of risk of working with them.

By identifying credit risks, you can take steps to protect your interests. You might choose to set stricter payment terms, request upfront payments, or simply avoid working with high-risk businesses altogether.

Credit checks provide valuable insights into the financial health of a company. You can uncover details such as outstanding debts, late payments, or legal notices that might indicate financial instability. By identifying these risks early on, you can make informed decisions.

When you work with companies that have a low credit score or poor credit history, you jeopardise your own cash flow. Credit checks can help you identify potential cash flow risks and enable you to implement strategies to mitigate them.

If you’re taking on new customers, you want to ensure they’re reliable and have a history of paying bills on time. Credit checks help identify whether a potential customer has a record of meeting their financial obligations, reducing the risk of non-payment and disputes down the road.

Credit checks can uncover red flags, such as a company's financial losses, a high level of debt, or a pattern of legal disputes. Recognising these warning signs early can help you avoid entering into risky partnerships that could harm your business.

Checking suppliers can reduce issues in your supply chain. If you spot a supplier in difficulty, you may want to work together to prevent the sudden loss of critical goods and services. Or you could diversify your suppliers to spread the risk.

When you credit check a company, you view a report of information that a credit bureau has gathered. Credit bureaus collect their data from various sources, such as Companies House, public records, financial statements, payment trends as reported from other companies and financial institutions, like banks.

All of the information on the report should give you an in depth insight into how financially stable a business is and how reliable they are at paying on time, based on this data.

You can easily check companies using your Capitalise for Business account. Here’s how the process works:

When reviewing a company's credit profile, look out for these red flags that may indicate financial instability or unreliability:

Consistently missing payment deadlines or defaulting on obligations can be a clear sign of financial distress.

Excessive debt relative to income or assets can indicate they’re not financially stable. They may struggle to keep up with their obligations to you on top of their existing debt.

Outstanding legal notices, such as a CCJ, demonstrate that the business has unresolved disputes and may have trouble meeting payments. A Gazette notice is a warning sign that the company will go into insolvency.

Checking company credit scores plays a critical part of an effective credit control process, in ensuring you're paid on time, reducing credit risks, and maintaining a healthy cash flow. Get started today with 20 free company credit checks.

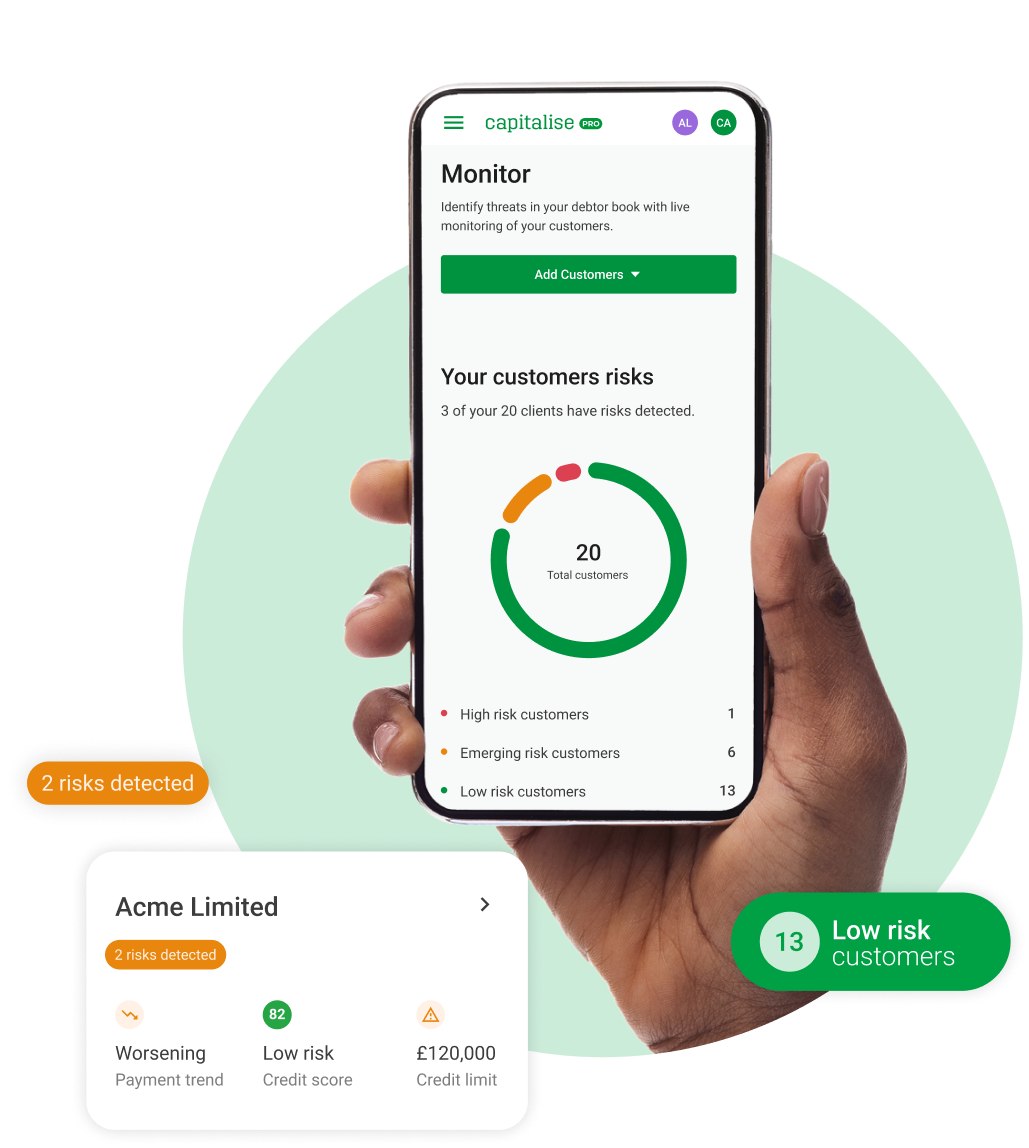

When you check a company with Capitalise, their credit report will show the following:

Business credit score

See their numerical and letter score, summarising the company's overall creditworthiness. The report will tell you whether this score is a high or low risk and whether extending credit would be a good idea.

Credit limit

View the company’s suggested credit limit and whether this has increased or decreased over time. You’ll be able to see if you’ve overextended to each customer.

Payment performance

This section provides a detailed account of the company's payment track record, including how many days over term they have paid historically. You will also be able to see whether their payment trends have been worsening, or improving.

Legal notices

Details of any legal notices registered against the company and whether these are resolved.

Credit factors

See which positive or negative factors are impacting the company's credit score.

Director details

Information about the company's directors, including their names and when they were appointed.

Financial summary

Financial statements, such as balance sheets and profit and loss statements, to offer insights into the company's financial health.

If you credit check a company and see adverse information, you might want to avoid working with them altogether to reduce risk to your business. However this won’t always be practical, especially if they’re a large client. You can still work with customers with low credit scores, but it's important that you take measures to protect your business. Here’s some strategies you can consider:

Requesting to be paid before delivering goods or services will reduce the risk of late or non-payment.

Requesting shorter payment periods, or reducing the amount of credit you offer can help to mitigate the risk.

Regularly reviewing the company's financial health and addressing any emerging risks quickly can help you navigate potential challenges.

Find out more about how you can work with companies with low credit scores.

If you run a company credit check on a new customer and they have a good business credit score, you can feel confident in offering them favourable credit terms as their risk of late payment is much lower. You may also want to offer them larger amounts of credit if you can comfortably do so.

You can find out more about how to work with companies with high credit scores.

Checking company credit scores plays a critical part of an effective credit control process, in ensuring you're paid on time, reducing credit risks, and maintaining a healthy cash flow. Get started today with 20 free company credit checks.

A good business credit score would be anything above 80/100, or an A or B credit rating. If a company has a good credit score, this suggests that they reliably pay on time and are in a financially stable position, so there is a low risk of working with them.

To check a company, once you sign up to Capitalise just put their company name or registration number into monitor. This will allow you to see all the information on the company’s credit report.

Yes, you can check another company’s credit score. This is an important step in an effective credit control process and will help a business to successfully assess the level of risk associated with a business.

Business credit scores are public information, so you don’t need permission to run a company credit check. As such, you could do this without the business knowing.

If your supplier has a CCJ, it can pose a risk to your business. This is because a CCJ is an early warning sign of insolvency, or financial instability, which could mean you could have disruption to the flow of goods or services to your business. Read more about what CCJs in your supply chain mean for your business.